.png)

.png)

April 11, 2025

The Lithography Inflection Point - How Two Different Approaches to EUV Could Reshape the Semiconductor Industry

By

Kristal Investment Desk

>

Newsletters>

Market Musings (17 – 21 March 2025) - The Price of Admission to the Golden Age: Uncertainty

The Price of Admission to the Golden Age: Uncertainty

The necessary discomfort of economic transition

The markets have entered what one might call a golden age of uncertainty. Since February, the Nasdaq is down about 10 per cent. Many components have fallen 20-30 per cent. Investors are skittish about tariffs, AI economics, and mixed signals from every direction.

One must hold two competing truths simultaneously: things are accelerating, yet much of the caution is warranted.

Consider the Trump administration's pending tariff decisions. On April 2, the White House will outline trading barriers for some 15 countries. Treasury Secretary Scott Bessett calls it "the American detox period" — a reset of fiscal and monetary balance with potential short-term pain.

But how much pain? The US currently collects about $65bn in tariff revenue. A moderate increase to $150bn might be absorbable; a leap to $1tn would almost certainly trigger recession. CEOs have adopted a wait-and-see approach, delaying investment decisions until the picture clarifies.

This economic uncertainty coincides with mixed macroeconomic signals. The Federal Reserve has adjusted forecasts downward, lowering GDP estimates from 2.1 per cent to 1.7 per cent, raising unemployment expectations, and increasing inflation projections. Consumer confidence is worsening, and airline bookings — often a leading indicator — show troubling weakness. Yet Bank of America reports consumer spending remains up 6% YoY. The economy appears simultaneously robust and fragile.

Investment managers have responded by reducing exposures to their bottom quartile while maintaining optimism about future opportunities. This "wait and see" approach, while seemingly passive, may represent the most rational response to the current environment.

For investors, three considerations merit attention:

1. First, uncertainty itself is being priced into markets, creating potential opportunities for those with longer time horizons. When others refuse to make commitments without perfect visibility, patient capital can secure favorable terms.

2. Second, the businesses positioned as "picks and shovels" providers to the AI gold rush — Nvidia chief among them — offer compelling risk-reward profiles relative to pure-play AI companies with unproven unit economics.

3. Finally, the fog will eventually clear. April's tariff announcements, continued earnings reports, and evolving AI business models will provide greater clarity on sustainable winners. Strategic patience while maintaining dry powder for deployment when visibility improves may prove the optimal approach.

The simultaneous presence of opportunity and uncertainty isn't an anomaly; it's the defining characteristic of every major economic transition. The golden age that follows will belong to those who can navigate this messy middle with discipline, embracing discomfort as the necessary price of admission to what comes next.

Powell signals calm amid the storm

Fed chair resists hawkish tilt despite tariff pressures and remains on course for cuts

The markets fret; Jerome Powell shrugs. As tariff threats loom and uncertainty rises, the Federal Reserve's decision to maintain rate-cut projections despite upwardly revised inflation forecasts sends a clear message: the economic noise will pass. Core PCE may rise to 2.8 per cent this year, but the central bank still expects a return to target by 2027.

Most telling was Powell's move to slow treasury balance sheet runoff from $25bn to $5bn monthly, addressing liquidity concerns when markets need stability. "Sentiment-based data looks a lot worse than what is actually playing out," he noted, drawing a sharp distinction between anxiety-driven surveys and economic realities.

Despite the clouds gathering—slower 2025 GDP growth of 1.7 per cent, slightly higher unemployment at 4.4 per cent—the Fed's medium-term outlook remains steady. The labour market shows resilience despite federal layoffs, and tariff effects are expected to prove transitory, as they did during the previous administration. For a central bank often accused of excessive caution, yesterday's steady hand amid swirling crosscurrents may represent Powell's most deft performance yet.

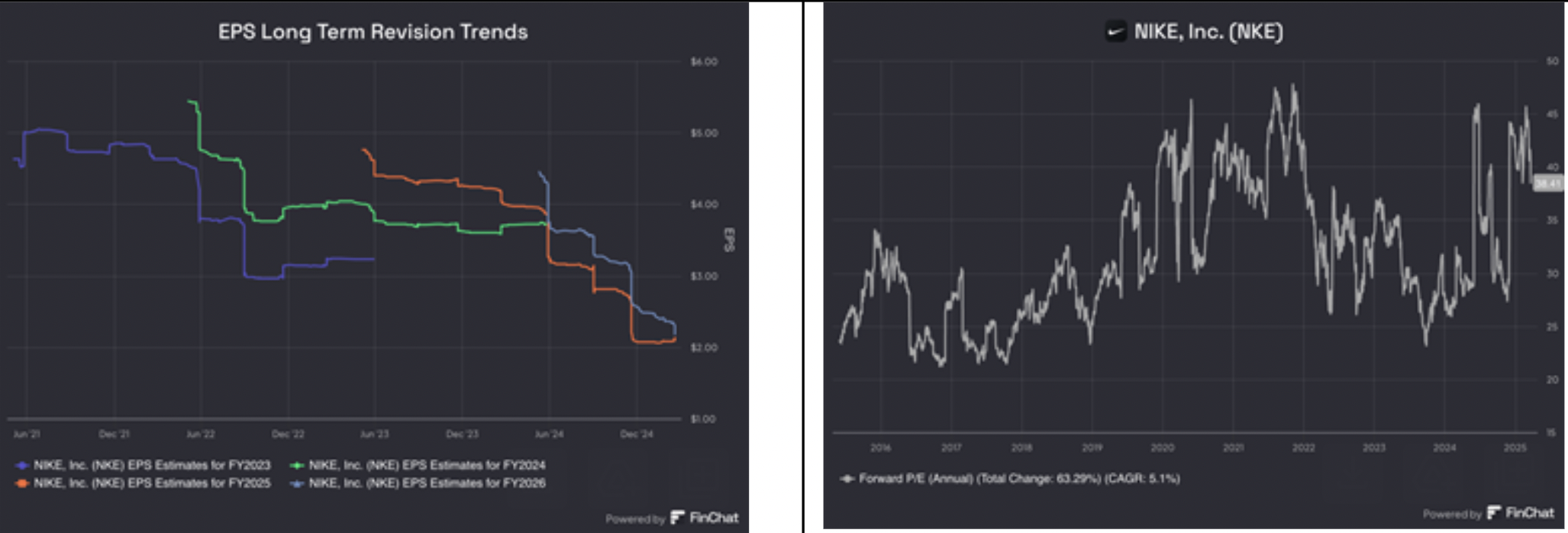

a. Nike: Running on Empty

Nike has hit the wall. Revenue fell 7% YoY as the sportswear giant's once-unassailable brand falters under the weight of poor execution. New chief executive Elliott Hill's "Win Now" strategy seems more aspirational than descriptive.

Core franchises like Air Force 1 and Air Jordan have grown stale. Aggressive digital discounting alienated wholesale partners. Now Nike must rebuild these relationships while simultaneously clearing excess inventory through outlet stores.

The company has slashed promotional days to zero in its digital channel versus 30 days in the same period last year, driving growth from positive in December to double-digit declines by February. Guidance of negative 13 per cent growth next quarter suggests more pain ahead.

At 38x NTM P/E — despite a projected 46 per cent earnings plunge this year — investors are paying for a recovery that remains distant. New launches like the Vomero 5 and upcoming Skims collaboration offer hope, but remain too small to offset core weaknesses.

Nike resembles an elite athlete who neglected training for years. For those expecting a quick sprint back to form, management's message is clear: this is an ultra-marathon.

b. Micron: Memory Boom Has Strong Legs

Micron Technology is riding high on computing's memory boom. The US chipmaker beat revenue estimates by 1.9% and EPS by nearly 10%. Investors can thank the company's prescient move into high-bandwidth memory (HBM), the critical component powering artificial intelligence hardware.

HBM revenue surged 50% QoQ to cross $1bn, suggesting Micron's bet on Gen AI's insatiable appetite for memory is paying off handsomely. The chipmaker is already sold out of HBM capacity for 2025 and seeing "strong demand" for 2026 supply. Not bad for a segment barely mentioned in earnings calls two years ago.

Nvidia, which uses Micron's HBM in its AI processors, provides a ready customer. Micron's 12-high HBM-3E offering, boasting superior power efficiency and memory capacity, will power Nvidia's Grace-Blackwell 300 system in late 2025. A third large customer is now receiving shipments.

But challenges persist in the company's traditional NAND business, where pricing pressure and underutilisation weighed on gross margins, which missed estimates by 40 basis points at 37.9%. NAND capacity is running 15% below cycle peaks as the company repurposes production lines for more profitable AI-focused chips.

At 11x NTM P/E, Micron trades at a substantial discount to the broader semiconductor sector. The memory maker expects earnings to grow 60% next year, after a 433% surge this year. Such volatility explains the discount. Memory remains cyclical despite the AI tailwind.

Micron's CEO Sanjay Mehrotra claims the company is in "the best competitive position in its history". The HBM boom, which Micron now estimates as a $35bn market, supports that optimism. But investors should remember that in semiconductor land, shortages inevitably become gluts. The trillion-dollar question is when — not if — that cycle turns.

c. Accenture: Steady digital steering through choppy waters

Accenture's message to the markets is clear: we are managing the transition in the US federal services business, but the digital transformation tide continues to rise. Shares in the consulting group fell 8% after its earnings release, suggesting investors remain skeptical.

The group reported revenues of $16.7bn, up 8.5% in local currency, with earnings per share of $2.82, a modest 2% increase. Full-year guidance was narrowed to 5-7% growth, removing the lower end of its previous range while trimming margin expansion expectations from 30 basis points to 10-20bps.

Beneath these numbers lies a tale of two businesses. The federal services unit, representing 8% of global revenue, faces uncertainty as the new administration reviews contracts with top consulting firms. Chief executive Julie Sweet acknowledged "many new procurement actions have slowed" but maintained a long-term optimism about modernizing government operations.

Meanwhile, the commercial business continues its steady transformation. Generative AI is emerging as a bright spot, with $1.4bn in quarterly bookings and $600m in revenue. First-half revenue from this segment has already surpassed the entire previous fiscal year.

The company's book-to-bill ratio sits at a healthy 1.3, with 32 clients signing deals exceeding $100m. This reflects Accenture's strategic pivot toward larger transformational projects rather than discretionary spending, which remains constrained.

At 24x NTM PE, Accenture trades at a premium to the broader market. This valuation suggests investors still believe in the secular digital transformation story, even as they digest near-term federal headwinds and moderating margin expansion. The real question is whether Accenture can continue justifying this premium through its Gen AI initiatives while navigating Washington's newfound parsimony. Sweet is betting it can.

d. FedEx: transformed networks await industrial recovery

FedEx's 3QFY25 results tell a tale of operational efficiency wrestling with economic headwinds. The logistics giant posted its first revenue increase this fiscal year at $22.2bn, while adjusted earnings of $4.51 per share missed estimates. Management has trimmed its full-year outlook to $18-$18.60 per share, the third consecutive guidance reduction, reflecting persistent uncertainty in the industrial economy.

The company's structural transformation continues apace, with $600m in cost savings this quarter through its DRIVE programme. Network 2.0 and Tricolor initiatives are delivering measurable improvements in aircraft utilization, with payloads up 9% and density improving 5% YoY. European operations, once a trouble spot, now show sequential progress in both service levels and profitability.

Yet industrial weakness remains the stubborn antagonist, pressuring high-margin B2B volumes that comprise 90% of freight revenue. With shares trading at roughly 13 times forward earnings, investors appear unconvinced about near-term catalysts. The company's thesis now rests on significant operating leverage when industrial activity eventually rebounds, with its leaner cost structure poised to capture outsized returns from recovery in priority services.

e. Carnival Corporation: Steady Sailing Through Choppy Waters

Investors have been abandoning ship at Carnival Corporation. The world's largest cruise operator has watched its shares sink more than 30 per cent from January highs despite this week delivering first-quarter results that handily beat expectations. The dichotomy highlights the market's neurosis about consumer discretionary spending in the face of potential economic headwinds.

The Miami-based company reported earnings per share of 13 cents — more than six times the consensus estimate. Revenue reached $5.8bn, exceeding forecasts even as operating margins expanded by 400 bps YoY. Such figures would normally prompt celebration, not trepidation.

So why is Carnival's stock being treated as if it has sprung a leak? The market, it seems, is paying more attention to storm clouds on the horizon than to the current calm seas. Fears of a mild recession later this year have prompted investors to extrapolate disaster for companies dependent on consumers' disposable income.

Yet Carnival's management is navigating these waters with a noticeably cautious hand on the tiller. Despite substantially beating first-quarter yield expectations (a key cruise metric combining occupancy and pricing) by 270bps, full-year yield guidance was raised by a mere 50 bps. That, combined with second-quarter EBITDA guidance below consensus expectations, suggests the company is deliberately building buffers against potential turbulence.

The conservatism is not entirely unwarranted. Discretionary travel typically suffers during economic contractions. But Carnival's current booking patterns reveal few signs of imminent demand destruction. Customer deposits sit at a record $7.5bn. Bookings for 2026 — well beyond any potential mild recession — reached an all-time high in the first quarter.

Moreover, unlike airlines or hotels, cruise operators benefit from a peculiar form of recession-resilience. Cruises offer a price-to-experience ratio that becomes increasingly attractive to value-seeking consumers during economic uncertainty. CEO Josh Weinstein noted, somewhat ruefully, that while the price gap with land-based alternatives represents "a big opportunity over the coming years," it also provides "a huge strength when people are looking to make their vacation dollars go even further."

Nevertheless, the company has undertaken sensible preparations for potential headwinds. Its DRIVE cost-saving programme continues yielding benefits. Debt has been reduced by over $8bn since its 2023 peak, with a further $5bn reduction planned through 2026. Average interest rates have declined to 4.6 per cent.

At roughly 14 times EV/EBIT, Carnival trades close to its historical average. If management's forecast of 12% return on invested capital materialises this year — reaching their 2026 target a year early — the valuation appears increasingly disconnected from fundamentals.

The company's share price suggests passengers are about to abandon ship en masse. The booking data indicates they are still eagerly lining up at the gangway. Only one of these narratives will prove correct. For investors willing to weather potential short-term volatility, current prices may offer an attractive point of embarkation.

· Alphabet Inc. (M&A): Google's reported $32 billion acquisition of cloud security vendor Wiz represents a strategic move into the high-growth cloud security space. Wiz, generating approximately $500 million in annual recurring revenue with ambitions to reach $1 billion this year, would strengthen Google Cloud Platform's security capabilities. While the 40x forward ARR multiple appears steep, it's reasonable given Wiz's 60% growth rate at scale and potential operational efficiencies under Google. The deal faces considerable regulatory hurdles, though Google's distant third-place position in cloud market share may help its case. If approved, the acquisition could add low single-digit percentage points to Alphabet's overall growth rate.

· The Trade Desk (TTD): The Trade Desk stumbled with its Kokai platform launch, resulting in disappointing results and guidance. CEO Jeff Green prioritized fixing user interface issues over meeting short-term financial targets, showing a focus on long-term reputation over quarterly numbers. Despite the setback, this is a fundamentally strong company now trading at approximately 32x forward FCF, and it’s possible for TTD to return to its 20%+ revenue and profit growth trajectory in the near future.

· Amazon: Amazon is strategically positioning itself in the AI chip market by offering steep discounts on its new Trainium chips compared to Nvidia GPUs, while simultaneously purchasing all available Nvidia chips. This dual approach allows Amazon to serve both premium and price-sensitive AI workloads. The company is targeting use cases where cost effectiveness matters more than maximum performance, creating a pragmatic alternative for customers who don't require Nvidia's top-tier capabilities. This strategy demonstrates Amazon's commitment to both developing in-house alternatives and maintaining strong partnerships with industry leaders like Nvidia.

· Nvidia GTC Conference: Jensen Huang's GTC keynote emphasized the exponential compute demands of agentic reasoning models, requiring 100x more processing power than traditional LLMs. Nvidia projected Blackwell GPU shipments of 3.6 million units in its first year, nearly triple Hopper's peak. The company unveiled "Dynamo," an open-source operating system for AI factories, and announced partnerships with T-Mobile, Cisco, GE Healthcare, CrowdStrike, and GM. Huang outlined Nvidia's product roadmap through 2027 and expanded robotics initiatives through its Omniverse platform. The company's comprehensive approach—providing GPUs, networking hardware, software tools, and industry-specific models—cements its position as the backbone of the AI revolution, with Huang predicting data center build-outs will reach $1 trillion "fairly soon."

Disclaimer: The views in the post are for for informational purposes only and should not be considered as investment advice. Please contact your RM or Kristal.AI for investment advise.

By

Kristal Advisors

March 25, 2025

Liked it?

Share it with your friends & colleagues!

April 11, 2025

By

Kristal Investment Desk

A fully digital onboarding process that can be completed within 15 minutes.

No more voluminous paperwork and queuing!

.svg)

We are licensed in Singapore, Hong Kong and India. Kristal Advisors (SG) Pte. Ltd. presently operates under the CMS license by the Monetary Authority of Singapore (MAS). Kristal Advisors (HK) Ltd is licensed and regulated by the Securities and Futures Commission (SFC) to carry out Type 4 and Type 9 regulated activities and is not involved in the discretionary management of any collective investment scheme. Kristal Advisors Private Ltd. presently operates as a Registered Investment Advisor under the jurisdiction of the Securities and Exchange Board of India (SEBI).

Read more about our privacy policy - Here

Copyright © 2023 Kristal Advisors (SG) Pte. Ltd. UEN: 201711235E

.png)

.png)

We are licensed in Singapore, Hong Kong and India. Kristal Advisors (SG) Pte. Ltd. presently operates under the CMS license by the Monetary Authority of Singapore (MAS). Kristal Advisors (HK) Ltd is licensed and regulated by the Securities and Futures Commission (SFC) to carry out Type 4 and Type 9 regulated activities and is not involved in the discretionary management of any collective investment scheme. Kristal Advisors Private Ltd. presently operates as a Registered Investment Advisor under the jurisdiction of the Securities and Exchange Board of India (SEBI).

Read more about our privacy policy - Here

Copyright © 2023 Kristal Advisors (SG) Pte. Ltd. UEN: 201711235E

WE ARE LICENSED IN SINGAPORE, HONG KONG, ABU DHABI, AND INDIA. KRISTAL ADVISORS (SG) PTE. LTD. PRESENTLY OPERATES UNDER THE CMS LICENSE BY THE MONETARY AUTHORITY OF SINGAPORE (MAS). KRISTAL ADVISORS (HK) LTD IS LICENSED AND REGULATED BY THE SECURITIES AND FUTURES COMMISSION (SFC) TO CARRY OUT TYPE 4 AND TYPE 9 REGULATED ACTIVITIES AND IS NOT INVOLVED IN THE DISCRETIONARY MANAGEMENT OF ANY COLLECTIVE INVESTMENT SCHEME. KRISTAL ADVISORS PRIVATE LTD. PRESENTLY OPERATES AS A REGISTERED INVESTMENT ADVISOR UNDER THE JURISDICTION OF THE SECURITIES AND EXCHANGE BOARD OF INDIA (SEBI). KRISTAL.AI MIDDLE EAST LIMITED IS LICENSED AND REGULATED BY THE FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) FOR CAT 3 A LICENSE.

Read more about our privacy policy - Here

Copyright © 2023 Kristal Advisors (SG) Pte. Ltd. UEN: 201711235E

USD 10,000

Minimum investment amount

ETF

Available Investment Products

Financial guide

Use while investing on Kristal

We encourage our India investors to use a financial guide. Kristal does not charge any additional fees for investing through them.

In case you already have a guide, we will try to bring them onboard. In case not, we can recommend one of our qualified partners to advise you through the journey.

I understand the financial products and would want to proceed with investing without a financial guide

ProceedIt is a structured product issued at par. In working it is similar to a Reverse Convertible but includes the barrier feature to protect downside to some extent. The underlying can be a basket of shares where the worst performing share may be delivered on expiry at the strike price.

Learn more about BRCs

It’s a structured product which is similar to ELONs, except the underlying can be a basket of stocks. This means that in addition to normal ELON factors, there are additional knock-out, knock-in rules associated with them.

Learn more about ELNs

An equity linked note which is issued

at par. The payment is made on initiation, by the client, in the form of shares that he/she might already hold and wants to unlock more returns especially during the periods when the stock is not giving any dividends.

Learn more about RELNs